The Covid-19 pandemic took us on one of the scariest rides of our lives, breaking up families and livelihoods globally. In fact, a 2020 survey reveals that 71% of UAE respondents are worried about living in the ‘new normal’. As a response, people are investing in healthcare measures, like signing up for a life insurance policy in the UAE.

Today, life insurance is necessary monetary protection and an emotional wellness measure for dealing with uncertain health risks.

Are you curious to explore the best life insurance in the country? Then, remember, it’s a two-step process.

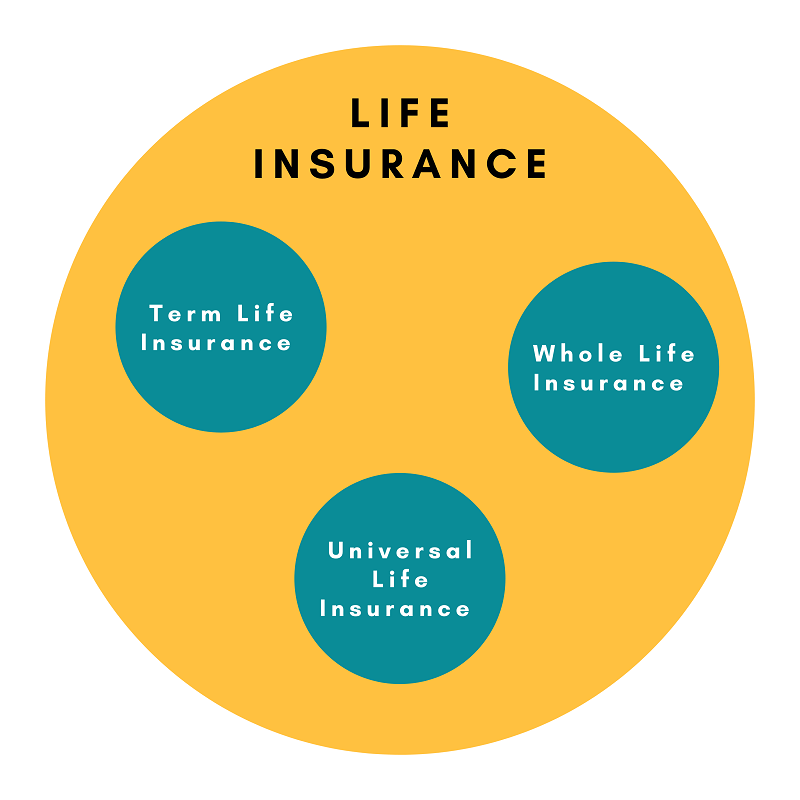

Step 1: Think of the life insurance industry as one big circle. This circle hosts several types of life insurance policies in the UAE.

Step 2: Your life stage, goals, investment value, and liabilities determine your policy options.

In this blog, I walk you through three life insurance policies in the UAE.

Types of Life Insurance Policy in the UAE

Whether you’re at the top of your health game, recovering from an illness, planning estate equalization, retirement planning, or building business legacies – it’s essential to have an insurance policy that protects your financial interests and provides maximum benefits at the right time.

Scroll down to access a quick crash course on the types of life insurance policies in the UAE.

1. Term Life Insurance

As the title indicates, term insurance provides coverage for a limited time, say 30 years, 50 years, and so on. Let’s understand this concept with an example.

Mathias is a 45-year healthy sales executive at an apparel company and has a family history of heart disease. As a protective measure, he signs up for a 20-year term insurance policy in Dubai to create a monetary cushion for his wife and children.

Now, jump to the future, Mathias will experience either of the two situations, which impacts the policy turnout:

Situation 1: Mathias lives a healthy life and celebrates his 65th birthday, the year his term insurance policy matures. Since he did not use the insurance in the last 20 years, the policy terminates, and he receives no benefit.

Situation 2: Mathias suffered a cardiac arrest at age 60 and passed away. His nominee (wife) receives the death benefit as a lump sum that she can use to restart her and her children’s lives.

Benefits of Buying Term Insurance in UAE

A. An inexpensive and straightforward life insurance policy that supports the dependents with getting independent in the absence of the policyholder’s death.

B. UAE does not charge tax on insurance payouts, allowing the grieving family an opportunity to make the most out of the death benefit.

Entry Eligibility: 18 – 65 years

2. Whole Life Insurance

If you’re comfortable investing in an expensive safety net that covers you for a lifetime in the UAE,

Whole Life Insurance is one way to proceed.

Stella, my 30-year old client, is a data scientist in Sharjah. Following my recommendation, she opted for a

whole life insurance policy worth $1 million. She assigned her husband as her nominee and is regular

with her premium payments annually.

The insurance provider divides her premium into three slabs – one covering the insurance cost, another

towards administrative fees, and the last building a cash value. Think of the cash value as an investment

fund, which grows over time at a flat interest rate.

So, for instance, if Stella wanted to make a partial withdrawal, get a policy loan, or sell off the policy – the

insurance provider will allow these transactions through the cash value. But, if Stella dies, the insurance

company will only provide her husband with the death benefit.

Advantages of Buying Whole Life Insurance in UAE

A. Provides extended coverage under a fixed premium value.

B. 0 tax on claiming the death benefit – encouraging a fresh start without significant financial troubles.

Entry Eligibility: 18 – 65 years

3. Universal Life Insurance

Do you want to exercise flexible control over your life insurance policy that covers you for your lifetime? In that case, Universal Life Insurance (UL) is a route to explore.

My client, Mark, a 45-year artist, signed a UL worth $2 million in Dubai. Like Stella, he has access to a cash value. But, here, his cash value’s growth depends on the insurer’s market performance. Mark can access the cash value:

● As loan collateral

● To surrender his policy

● For meeting future premiums

HNIs like Mark can also use a UL for estate planning, where the policy value will equalize asset division

between heirs. Here’s an interesting case study of Zaid in this context.

Benefits of Buying Universal Life Insurance in UAE

A. Lifetime coverage under a flexible setup.

B. Assists in estate planning.

C. Access to cash value provides financial support during unemployment/retirement stages.

Don’t Skip Critical Illness Coverage

Regardless of the life insurance policy you sign up for in the UAE, I strongly recommend adding critical

illness coverage as a policy add-on. Today, everything may be great. Yet, the rising risks of lifestyle

diseases and high treatments costs will fire up your pockets in the absence of life insurance.

I’m sure you agree that financial stress is the last thing one wants during recovery, especially if it boils

down to taking an unpaid break from work. Here, the critical illness coverage will fulfill the financial

obligations during the diagnosis and post-recovery phases. Covering 35 – 40 major conditions, sigh a

breath of relief with a one-time cash benefit in hand while focusing on getting and feeling better.

Discover: Why Critical Illness is the Need of the Hour?

Explore the Best Life Insurance Policies in the UAE

Associating your money with a life insurance policy is one of the most crucial decisions of your life –

making it essential to evaluate your options critically. While each policy has its benefits, your best fit

depends on ‘when’ you sign up and the kind of risks you wish to cover.