Guide to Retirement Planning in UAE

It’s never too late to plan for your Retirement!

“Retirement is not the end of a road, it is the beginning of an open highway.”

Retirement is a blissful stage of life for which you have been working for decades-no professional worries, no deadlines, no reporting hours, no bosses, few commitments and little need to work for money. It’s spending the rest of your lives doing what makes you happy and content.

But the reality is that more and more people, are working into their late 60s and 70s, because they did not plan well enough for this.

Life expectancy is constantly going up, but fewer people are getting pensions. This means you must be able to fund your own retirement. Moreover, inflation is a significant factor that can cause your current expenses to significantly rise by the time you retire. If you intend to hang your boots in the next ten years, start your retirement planning in UAE right away. You can follow this step-wise approach and find answers to the most pertinent questions.

What are your retirement goals?

You must constantly revisit your retirement goals. You may want to take that desired holiday, pursue a hobby, adopt a certain lifestyle, or move to an island paradise. It would help if you were specific about your goals and classify them as short-term, medium-term, and long-term. Each goal is unique and would require different financial preparations. Hence, it would be best if you considered them thoroughly before designing your retirement plan.

Where do you start?

At this stage, you must draw your retirement planning budget. For that, you must take all your current financial commitments, regular expenditures, as well as housing expenses into account.

Medical Costs: Once you reach the 60s healthcare costs can be significant. Hence you must revisit your Health covers and assess whether you want to go for a Critical Illness cover if you don’t have one already. If you wish to go for a Critical Illness policy, act quickly else the premiums will be higher, or insurers may not be willing to provide you with a cover.

Retirement Income: After looking at your expenses, it’s time to looks at your retirement income. Your predictable income from social security, pensions, as well as your withdrawals from your pension account can be classified under this head. If you are planning to earn through other means after your retirement, write down those income streams too, and plan for them. You may need to invest in yourself, to pursue that long-lost passion you have had since childhood.

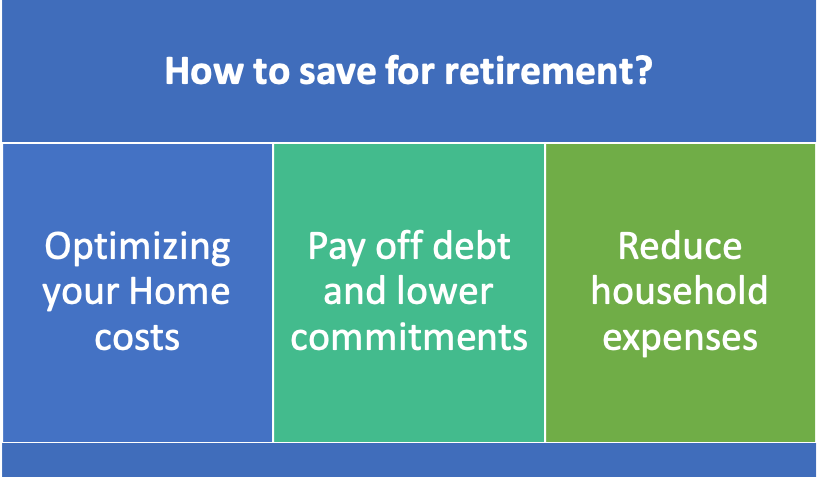

How to Save For Retirement Planning in UAE?

To ensure that you have a significant retirement corpus, you must start taking measures to save as much money as possible.

Optimizing your housing expenses: If you plan to retire shortly, you may consider shifting to a home that will not cost you a fortune to maintain. This will free up a lot of your expenses while you can save for your retirement. It is also important that you decide where exactly you would want to live, when you retire.

Paying off Debt: The last thing on your mind would be to retire with a huge debt burden. Without a regular paycheck, it will be challenging to repay loans. You should also pay off any life insurance premiums while you are working as small insurance premiums can be a drain when you retireSince you still have a regular income now, you can accelerate the repayments to an extent feasible to you. Another important thing would be to steer clear of acquiring any additional debt.

Lower household expenses: It may sound trivial, but a more reasonable way of living at this stage will go a long way in ensuring a secure retired life. Retirees are often immensely impacted by inflation as they live on a limited income. While pension income would remain constant, prices would continue to rise. Fortunately, we live in the age of e-commerce, and there are plenty of ways to save on daily essentials today. This will help you invest more money towards your retirement.

Where to invest the savings?

Saving money for retirement is one side of the coin. To increase financial security, you also need to invest.

Increase retirement Contributions: It is wise to check if you can raise your retirement contributions in your pensions or any other plan you currently have.

And if you have not planned, it is good to start now.

Discuss your options with a financial advisor or professional.

Build a diversified portfolio: To enjoy a peaceful retired life, and keep financial concerns at bay, consider building a diversified portfolio. A well-balanced or diversified portfolio includes equity, bonds, mutual funds, and other assets that offer long-term growth prospects. As you age, your risk appetite declines.

However, while you are saving, it is advisable to take a higher exposure in equities and take on more risk, as you are putting away smaller amounts towards your retirement. If you want to explore this, again it is best to talk to a financial advisor.

How much do you need to retire: As a thumb rule, you should follow the 4% rule in my opinion. This means that if you need $100,000 for your living expenses per annum, you should have saved up $2.5 million.

2.5 million invested in conservative, income generating instruments can generate close to 4% returns, which can take care of your living expenses. Of course there will be volatility in your capital and income over time, but this is a simplistic way of looking at a target fund.

Better late than never

If your retirement is just a decade from now, you may feel it is too late to plan anything. However, for investment, it is never too late to get started. Be sure to set goals that are realistic and adopt a pragmatic approach. Even if you start taking measures now, you can create substantial retirement savings.